Energy Markets: Winter is coming

The Energy Markets in August continued unseasonably high pricing

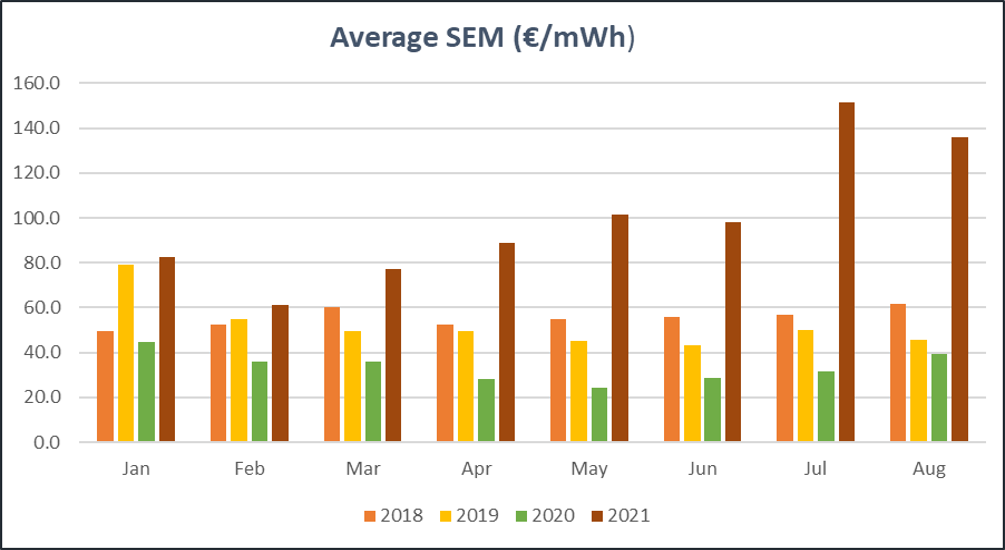

Average power prices pegged back slightly off July’s record highs. In August 2021, they averaged €136 per mWh, up over 3 fold on the same period in 2020 and 10% decrease on the previous month. Prices have remained unseasonably high versus similar periods since iSEM commenced in Oct 2018.

We saw this level of pricing in August for the following reasons:

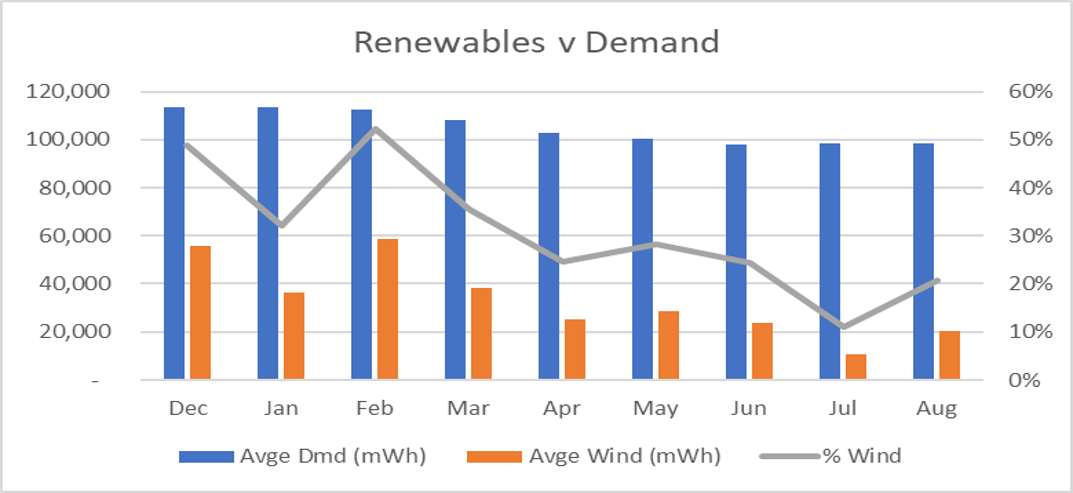

- Wind generation contributed 21% of the generation mix, up 90% on July, but stubbornly low.

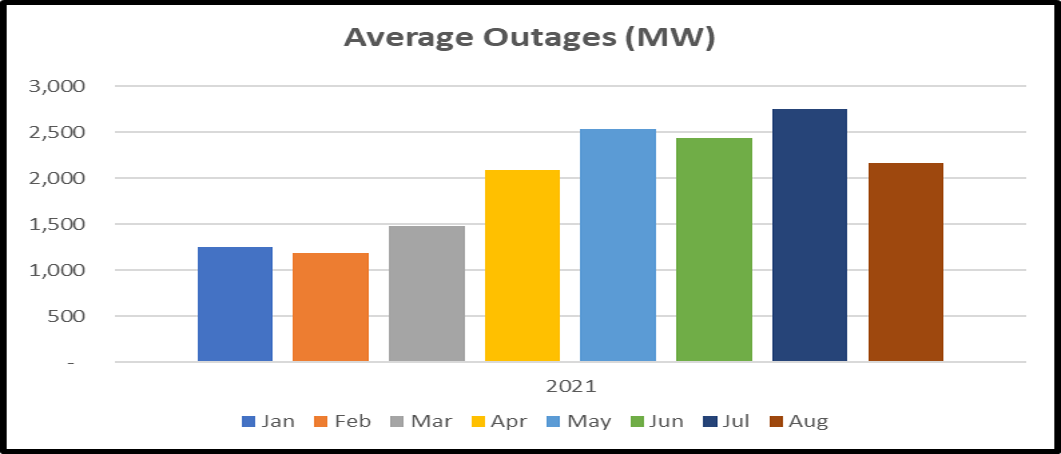

- Unscheduled Outages remain at some key key Combined Cycle Gas Turbine (CCGT) generation plants (e.g. Whitegate 440MW,Huntstown 400MW). Overall average outages for August decreased by 21% on July at 2.15GW.

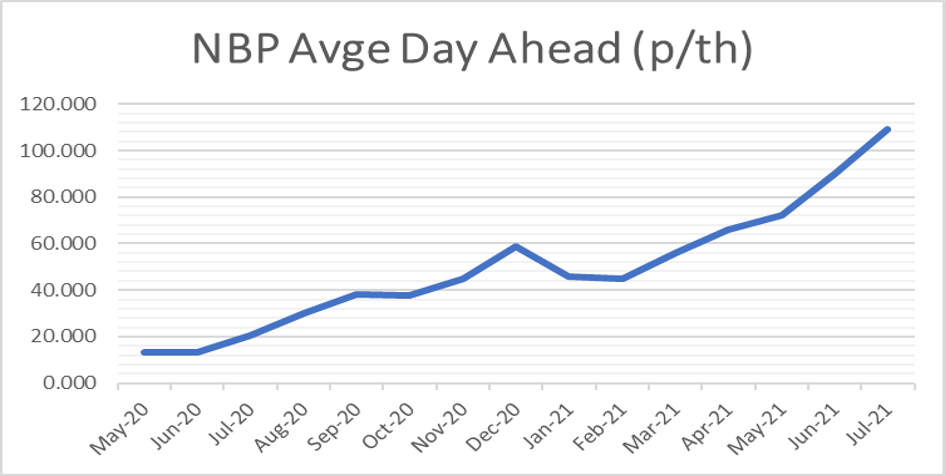

- Day ahead Gas prices continued their seemingly non stop spiral to record highs

- Prices crashed past the £1/th milestone, averaged 109p/th, up 21% on July averages and over 400% on the prior year.

Gas

- LNG deliveries to Europe remained weak due to strong demand and better prices available in Asia.

- Replenishing European storage has remained sluggish. While UK storage is 80% full, its lowest since 2017, European storage is only 62% full.

- Further storage injections will further boost gas prices.

- The positive news about the Nord Stream 2 pipeline imminently opening waned as uncertainty about volumes and the date of EU approval remained.

Carbon

- Carbon prices traded upwards above €60/tonne level in August.

Coal

- Coal prices increased further as increasing gas prices has brought coal based generation higher in the merit order for power.

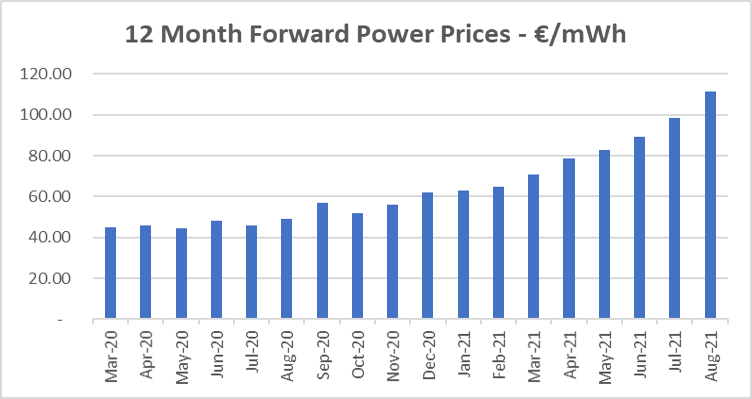

What’s next?

12 months forward prices continue to increase each month in 2021. Why?

- On going support for gas prices as gas storage levels in Europe are replenished at great speed in advance of Winter.

- High gas demand in Asia

- Significantly, continued outages in key Irish power stations are expected to continue throughout 2021.

Disclaimer

The contents of this report are provided solely as an information guide. The report is presented to you “as is” and may or may not be correct, current, accurate or complete. While every effort is made in preparing material for publication no responsibility is accepted by or on behalf of New Measured Power Limited t/a Pinergy for any errors, omissions or misleading statements within this report. No representation or warranty, express or implied, is made or liability accepted in relation to the accuracy or completeness of the information contained in this report. New Measured Power Limited t/a Pinergy reserves the right at any time to revise, amend, alter or delete the information provided in this report.