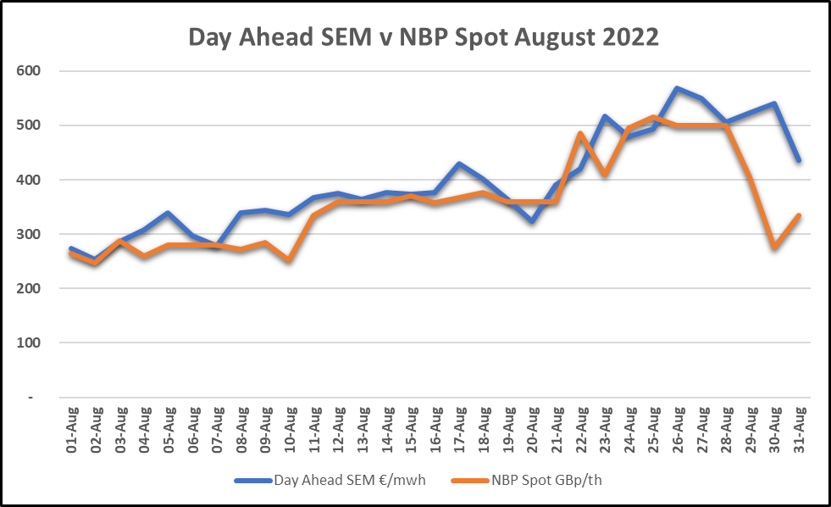

The upward trend in average power prices seen in July continued throughout most of August. As the spot NBP (gas) price increased, the Day Ahead Single Energy Market (SEM) wholesale power price followed suit.

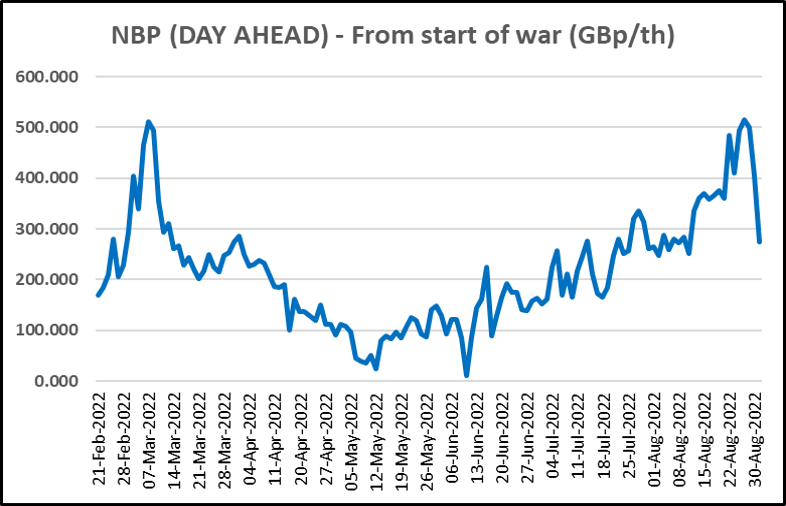

A steady increase in the NBP price for the first 28 days of August was followed by a sharp decline as Germany announced that it was feeling comfortable about its gas storage situation ahead of winter. This allowed some hope of abating energy prices for the last few days of the month.

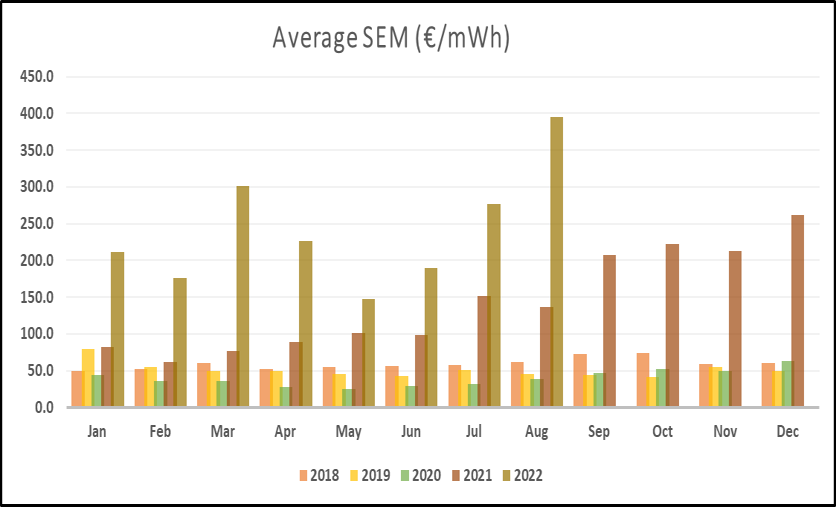

On average, prices increased by 42% month-on-month, with August’s outturn being €394/mwh, compared to €277 in July, setting new record levels on the Day Ahead SEM price.

1. High volatility with a general upward tick for Gas prices

- High volatility with a general upward tick, in line with market behaviour seen in July, prevailed again in August across gas European markets.

- Fuelling that push toward higher prices, is increased concern over the security of gas supply from Russia. Gas supplies have decreased by up to 80% on key routes since mid June. The ongoing shenanigans around the critical Nord Stream 1 pipeline, which shut down completely for maintenance at the end of August, suggests that Russia may be willing to manipulate the supply of energy to suit their agenda.

- As the European Commission return from their traditional August holiday period, there are strong signals that the impact of runaway gas prices on the cost of energy is going to be addressed urgently.

- Germany’s positive announcement around gas storage levels and energy security brought some price relief toward the end of the month. However, the market remains on tenterhooks and is likely to react negatively to any further curbs on Russian gas supply.

- Europe continues to import record volumes of LNG (Liquid Natural Gas) in 2022 and LNG volumes have surpassed Russian gas flows since June.

- The re-opening of the Freeport LNG terminal in Texas, a significant source LNG supply from the US to Europe, has been further delayed and is now not expected to come back online until early to mid November.

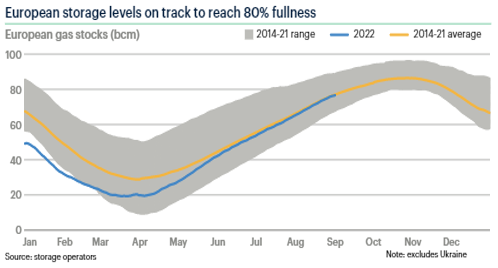

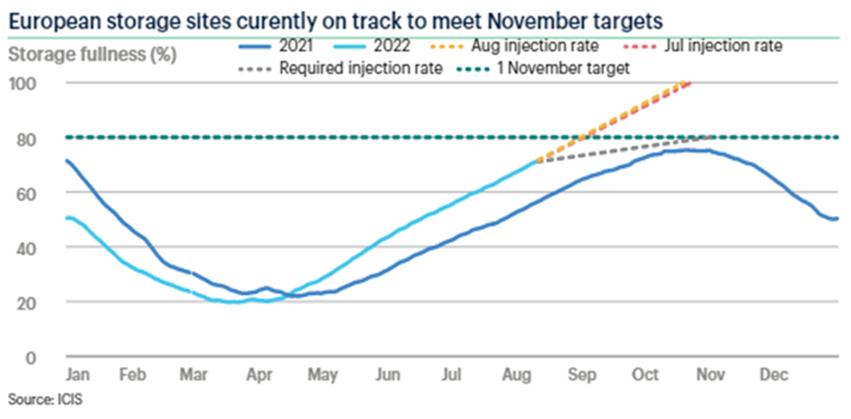

- European aggregated storage sites were just below 80% of full capacity on 1 September, which was the target mandated by the European Commission.

- Storage injection rates have been high through July and August. This has added significant upward pressure on gas prices.

2. Wind generation needed to keep pricing in check

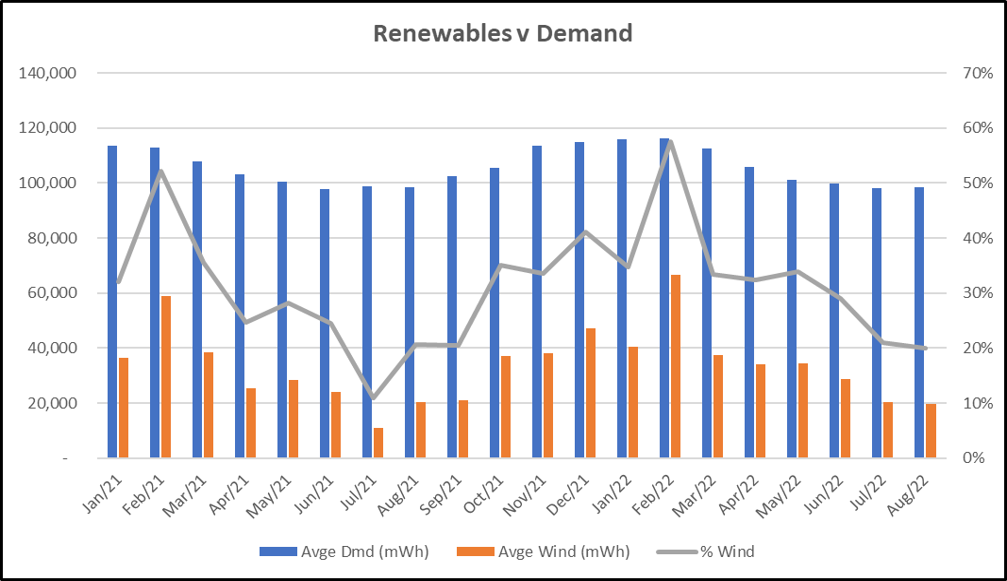

- Renewables, in the form of wind, contributed 20% of the generation Mix in August, a reasonable contribution for this time of year.

- However, more wind generation is desperately needed to help keep Irish power prices down.

3. Amber alerts returned in August

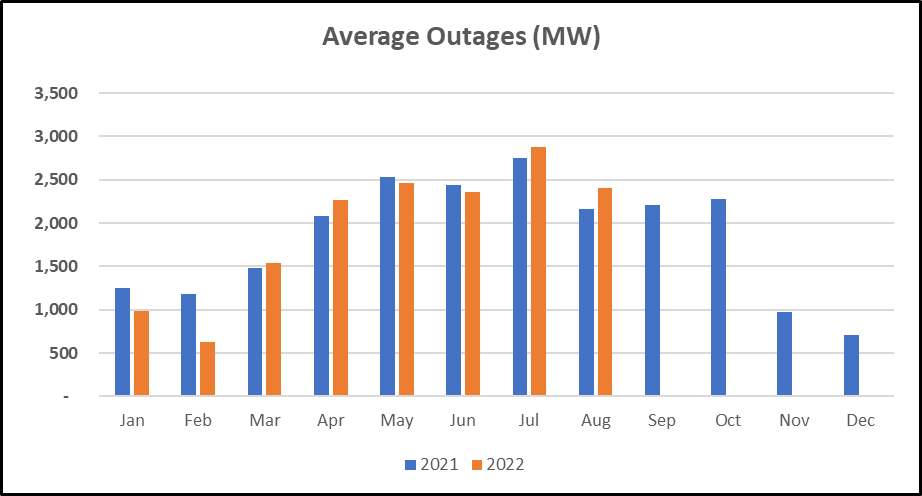

- Outages are in line with those experienced during the 2021 Capacity Crisis and the number of amber alerts has increased in August.

- However, the majority of outages in August were planned, with the exception of Dublin Bay (415MW) & Tarbert (243MW), which are forecast to come back on line in early August and by March 2023 respectively, and a number of other shorter outages which were mostly back online before the end of August.

- It is hoped that such a crisis will be averted later this year.

What’s next?

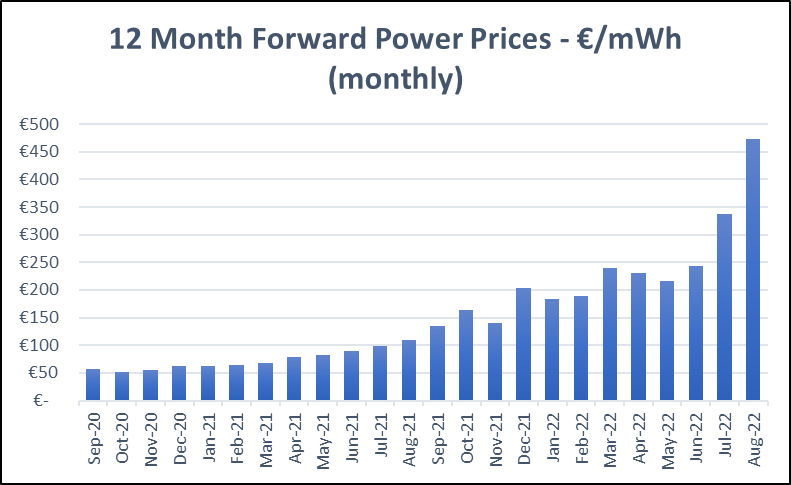

- Power Forward prices in the Irish market have reached record levels in August.

- The uncertainty over the security of Russian gas supply going into winter 2022/23, and general chaos in gas markets, has bumped up the risk premium, thus impacting the forward price of energy in Ireland and elsewhere.

- The reduced gas supply coupled with the breakout of war, European sanctions and markets fear of further sanctions against Russian energy exports has added to that increased risk premium in forward pricing.

12 month forecast

- The EU Council has signaled they are ready to take emergency measures to help with the soaring cost of energy bills. Potentially positive if correctly actioned.

- Geopolitical situation in Ukraine and potential for Russia to influence the gas market: Negative

- Europe continues to import record volumes of LNG in 2022, with some nations, such as Germany, pushing through the development of new LNG terminals: Positive

- Moral and Political demand for sanctions on gas and oil – Negative

- Storage: At the end of August, European storage sites appeared to be on target to meet increased requirements ahead of winter: Positive

- Vulnerability of the already strained and highly sensitive global gas supply to any further negative influencing factors such as the perceived manipulation of supply by Russia: Negative

Disclaimer

The contents of this report are provided solely as an information guide. The report is presented to you “as is” and may or may not be correct, current, accurate or complete. While every effort is made in preparing material for publication no responsibility is accepted by or on behalf of New Measured Power Limited t/a Pinergy for any errors, omissions or misleading statements within this report. No representation or warranty, express or implied, is made or liability accepted in relation to the accuracy or completeness of the information contained in this report. New Measured Power Limited t/a Pinergy reserves the right at any time to revise, amend, alter or delete the information provided in this report.