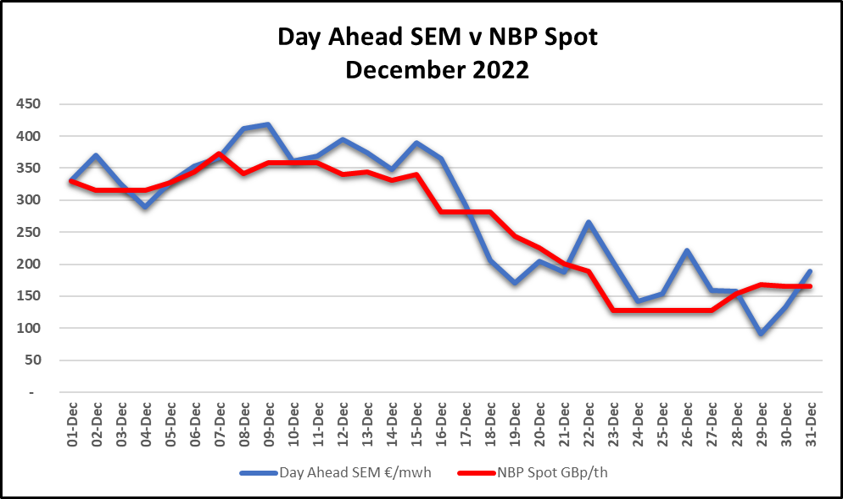

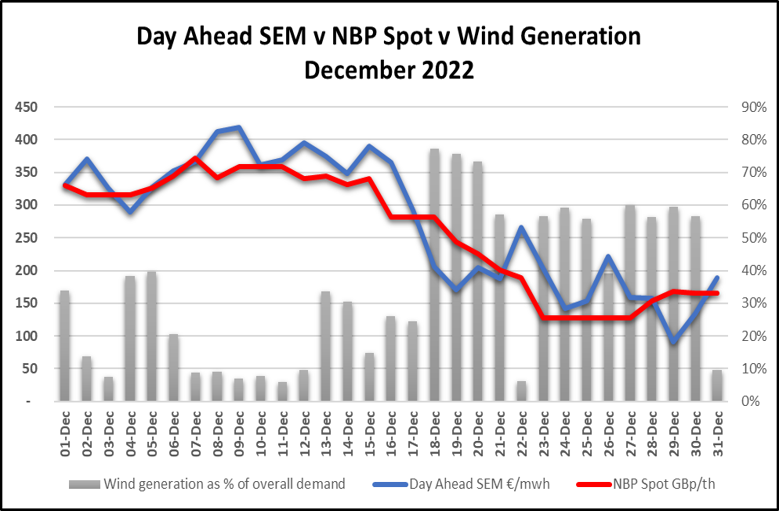

Virtually non existent wind and severely cold temperatures resulted in extremely high power prices in Ireland during the first 2 weeks of December.

The latter part of the month saw prices drop steeply again as demand reduced over the holiday period and wind generation in the Irish grid picked up.

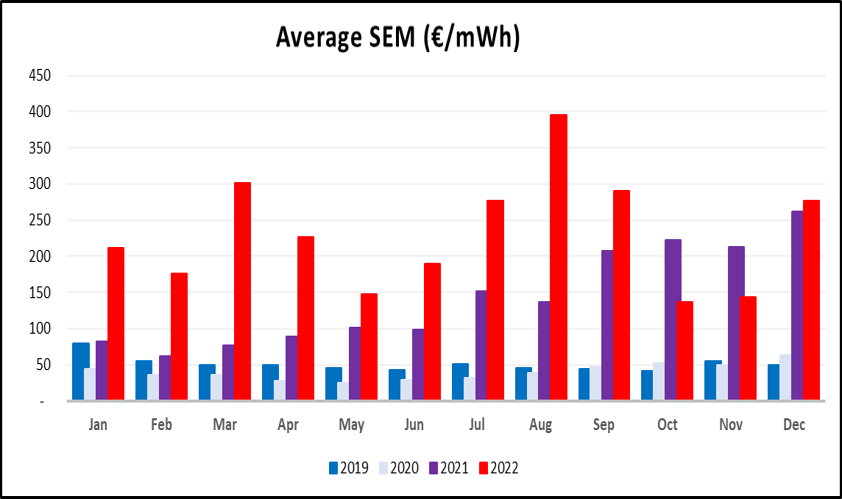

On average, prices in the SEM Day Ahead market almost doubled month-on-month, increasing by 94%. December’s outturn was €277/MWh, compared to €143 in November.

The NBP spot market was also impacted by the threat of a colder than expected winter in the early part of the month. Gas prices soared, bringing a stark reminder that high levels of volatility remain in the system.

As milder, windier, weather forecasts began to emerge, NBP prompt contracts fell, bringing Irish power prices along with them.

1. The cold snap prompted significant increases in Gas consumption

Pricing and Supply

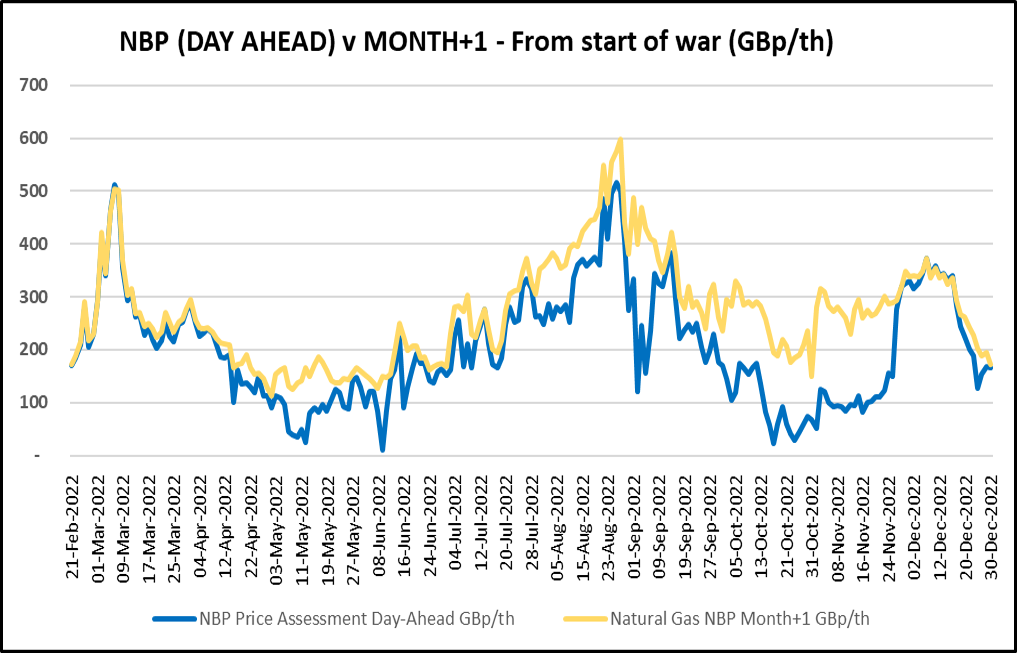

- The cold snap at the end of November and the first half of December, naturally, lead to a significant increase in gas consumption and the fear of a colder than expected winter. This triggered a steep climb in NBP prompt and future contracts.

- Showing how quickly market sentiment can swing in these unsure times; as soon as the cold weather abated and more favourable weather forecasts for Q1 2023 started to emerge, European gas prices, including the NBP, tumbled all along the curve.

Storage and Consumption

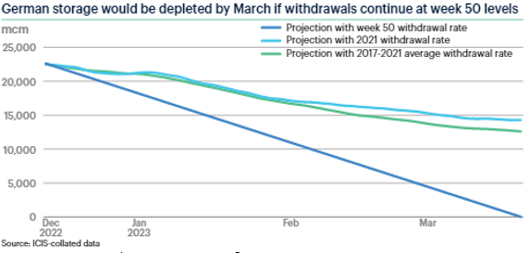

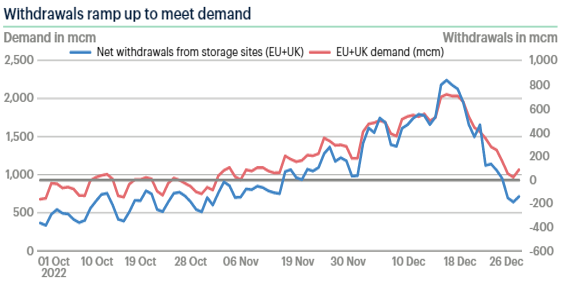

- As mentioned above, the cold snap and resulting increased gas consumption in early December sparked panic in the markets, with predictions that withdrawals could not be maintained at such levels (see graph below).

- However, the high level of withdrawals in week 50 may well have been connected to the high spot prices at that time, which would have encouraged the use of any lower cost gas in storage.

- As the graph below shows, storage withdrawals dropped considerably in late December, as spot prices fell and demand decreased for the holiday period.

- Now that spot prices have fallen and temperatures and wind levels have picked up, this should give EU member states the opportunity to rebalance injections and withdrawals somewhat, helping to meet storage targets as the winter progresses.

Positivity across the European grid

- Many eyes were on the French grid during December, where several Nuclear power Generation sites, which had been out of action due to maintenance, came back online just as the cold snap hit.

- The success of these Nuclear sites, and the potential for France to be re-established as a net exporter of energy was welcome news to European gas markets. France has increased reliance on gas while its Nuclear fleet was underproducing in 2022, significantly adding to overall gas demand on the continent.

- Another key element in the European power grid is the availability of Norwegian pipeline gas.

- The Norwegian government sent out positive signals in December, noting that it’s grid will be well stocked with Hydro power this winter and spring.

- This bodes well for availability of much needed gas supply to the UK and the European continent.

- Significant break throughs in grid supply such as the above have notable impacts on power pricing within the European grid.

- The big question now is whether Europe (and the UK) can manage power consumption over this winter period. Any threat to gas inventories will surely send prices further upwards.

EU making progress?

- The EU has been accused of not acting quickly enough during this (now 15+ months long) energy crisis and only tinkering around the edges when it comes to necessary market reform.

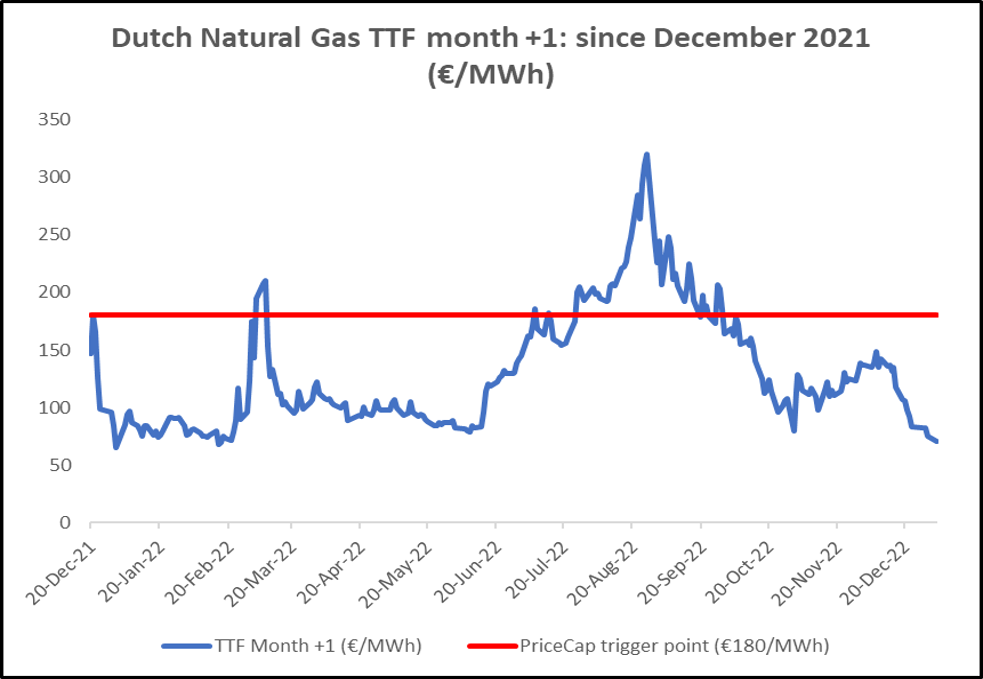

- On 19th December, after months of deliberation, the EU Commission announced that a gas price cap mechanism had been agreed upon by member states.

- Key to getting agreement from opponents to the price cap, was a number of get out clauses, that can activate if the mechanism looks to be threatening security of gas supply, or the integrity of the European energy markets.

- Regardless of whether the mechanism is ever triggered (which we believe is unlikely), it is hoped that the presence of a cap will achieve a balance between bringing some calm to power markets while not impeding flows of gas into the continent. Watch this space!

- The main trigger point for the gas price cap, would be if the TTF month ahead contract breaches the €180/MWh level for 3 days in a row. The graph below shows when this level has been breached since December 2021.

- There are also a number of other criteria that must be met, in order to trigger the price cap, and the mechanism looks set to closely follow international LNG pricing.

- It is hoped that some meaningful market reform can be achieved in 2023, including the introduction of an new LNG pricing benchmark which better represents the new gas mix in the continent, that has evolved since the necessary switch from Russian pipeline gas to LNG deliveries in 2022.

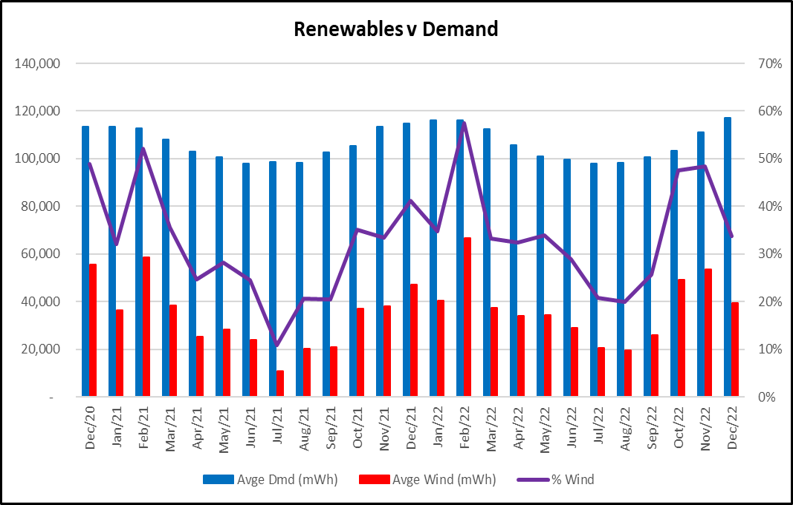

2. Renewables contributed 34% of the December mix

- Renewables, in the form of wind, contributed 34% of the Generation Mix in December; significantly lower than the same month in 2021 and 2020.

- As usual, availability of renewable generation had a significant impact on power prices in December.

- The graph below shows that when wind generation was down during the month, the wholesale cost of power was generally up, and vice versa.

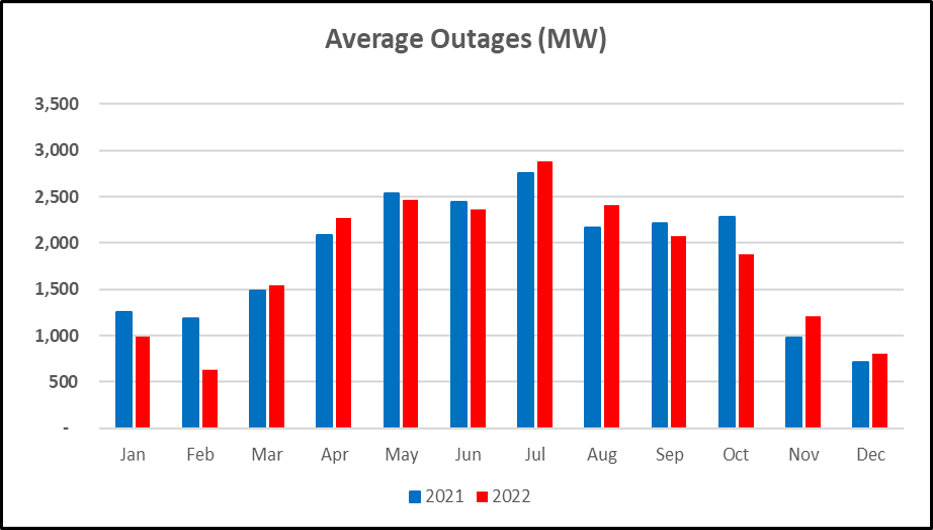

3. Outages remain manageable on the Irish grid

- Although there have been a number of Amber alerts on the grid during 2022, outages were maintained at manageable level throughout the year.

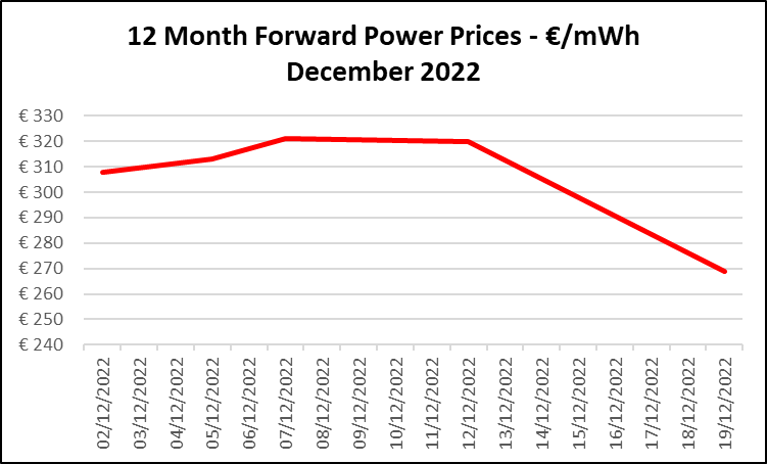

- Forward pricing continued to increase worryingly in the first 2 weeks of the month, picking up the trend from late November.

- Then, as we have seen so frequently throughout 2022, that trend switched dramatically and forward pricing fell significantly in the later part of December.

- Although December averages returned high, the trend in power futures was most certainly downward before we reached the holiday period.

- While all decent people long for an end to the dreadful war in Ukraine as soon as possible in 2023, unfortunately the end is not yet in sight. As the war and myriad other influencing geopolitical factors remain in play, it can be assumed that a high level of risk premium remains in the near future.

12 month forecast

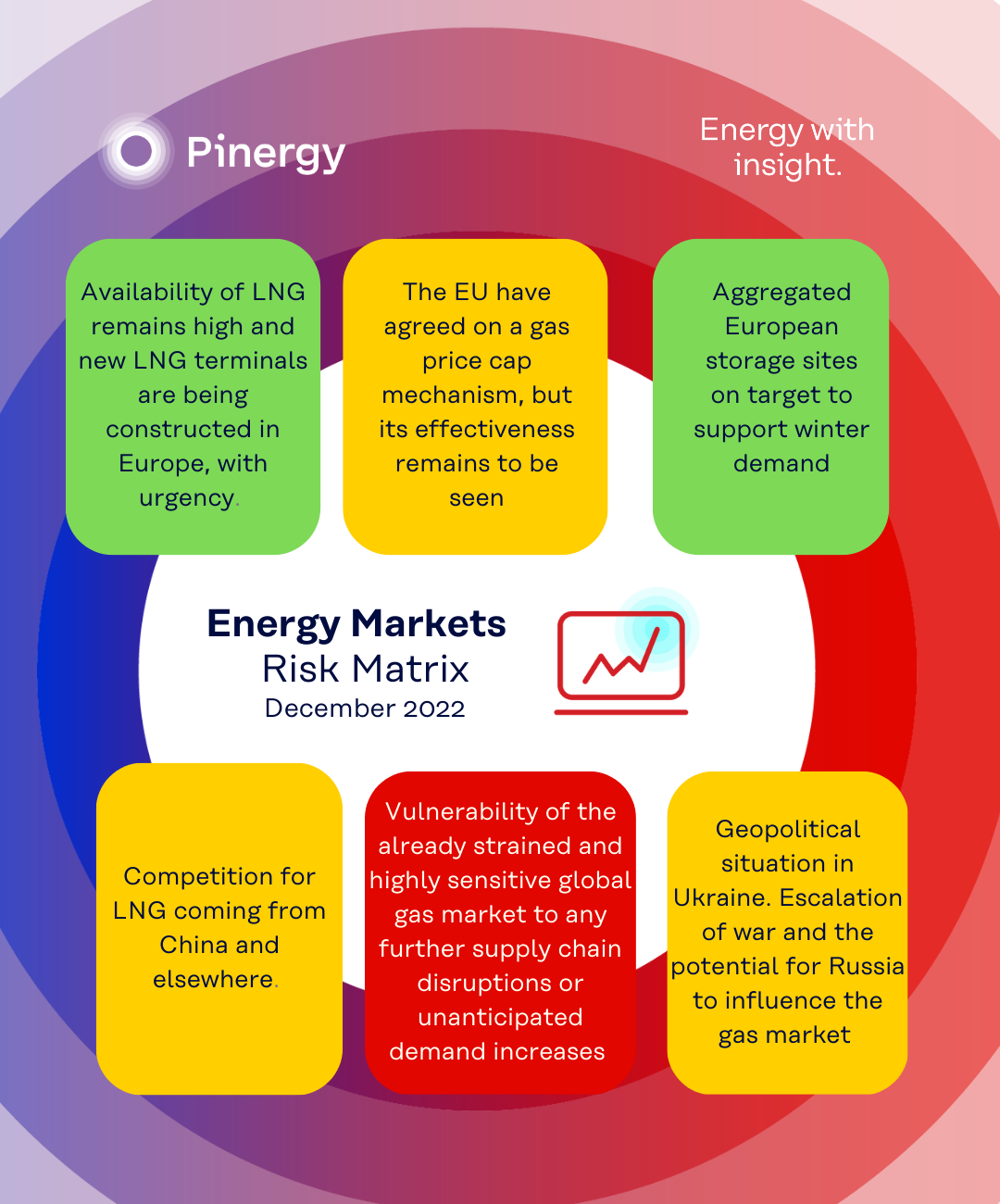

We have compiled a list of the key factors we feel have the highest potential to influence power prices over the coming 12 months and rated as follows:

Green = Price reducing impact and highly probable.

Amber = Risk of increased power prices and of lower concern.

Red = Significant risk to 12 month forward price outlook, with medium to high probability.

Although the winter weather outlook is looking much better than it was in early December, volatility remains in both the markets and the climate.

Although no month remains the same in the energy markets these days, we feel the risk level of increasing energy prices over the next 12 months is more or less where it was last month

Disclaimer

The contents of this report are provided solely as an information guide. The report is presented to you “as is” and may or may not be correct, current, accurate or complete. While every effort is made in preparing material for publication no responsibility is accepted by or on behalf of New Measured Power Limited t/a Pinergy for any errors, omissions or misleading statements within this report. No representation or warranty, express or implied, is made or liability accepted in relation to the accuracy or completeness of the information contained in this report. New Measured Power Limited t/a Pinergy reserves the right at any time to revise, amend, alter or delete the information provided in this report.