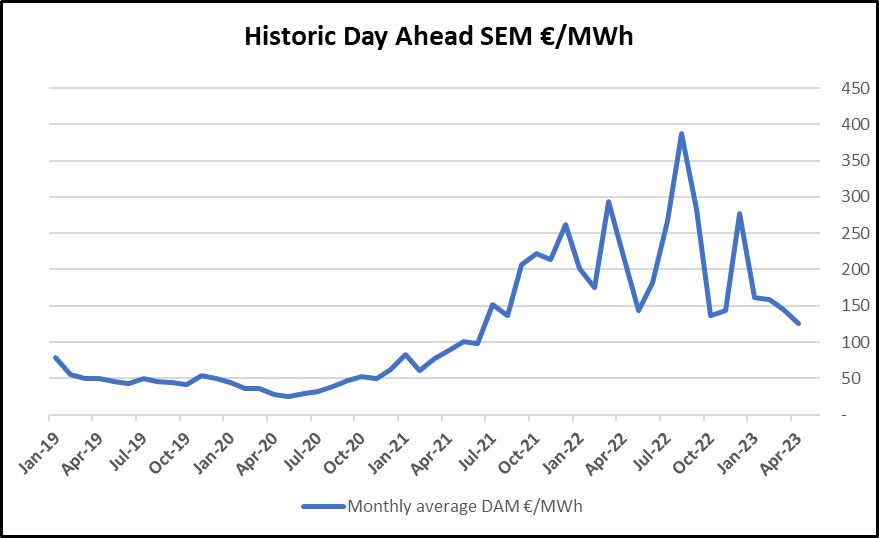

Average power prices have fallen every month in 2023 so far. Average prices in the SEM Day Ahead fell ~13.5% month-on-month. April outturn was €126/MWh, compared to €145 in March.

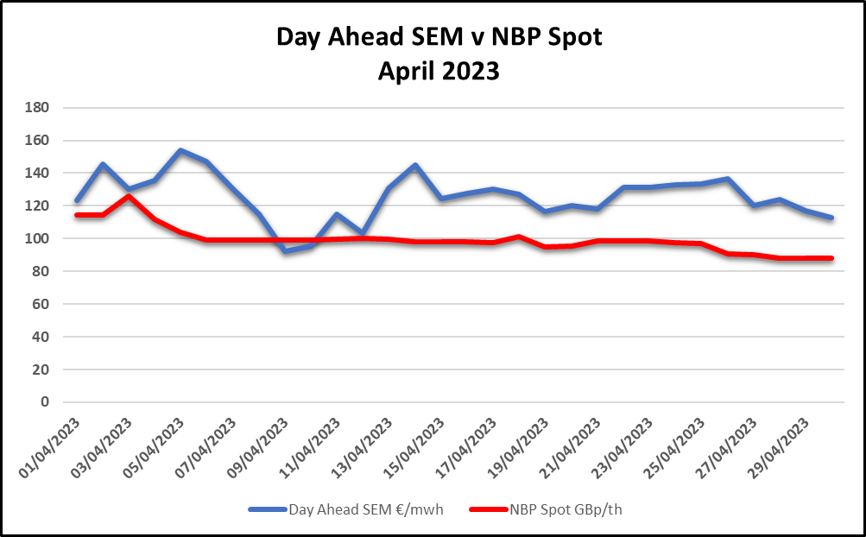

British gas prices fell consistently across the month. However those gas prices remain at historical highs and the reliance on British gas for the large majority of Irish grid power has meant that Energy prices in Ireland have remained amongst the highest Europe in 2023.

Gas – Pricing & Supply

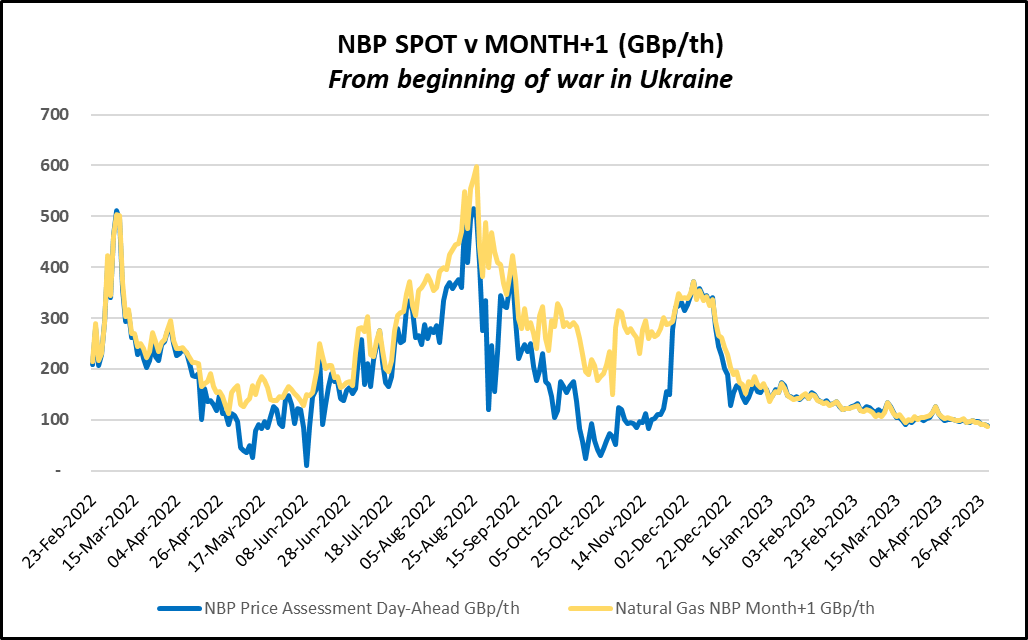

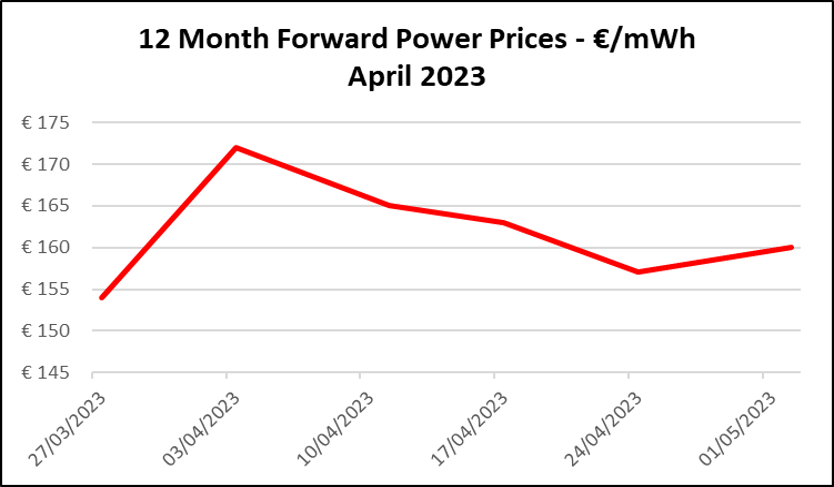

- NBP near curve price volatility was muted in April, while prices continued to decline, as can be seen in the graph below.

- Prices for 2023 gas deliveries remain elevated but a heavier weighting of risk has now shifted to 2024 contracts. We will explore this trend later in the review.

Gas – Consumption & Storage

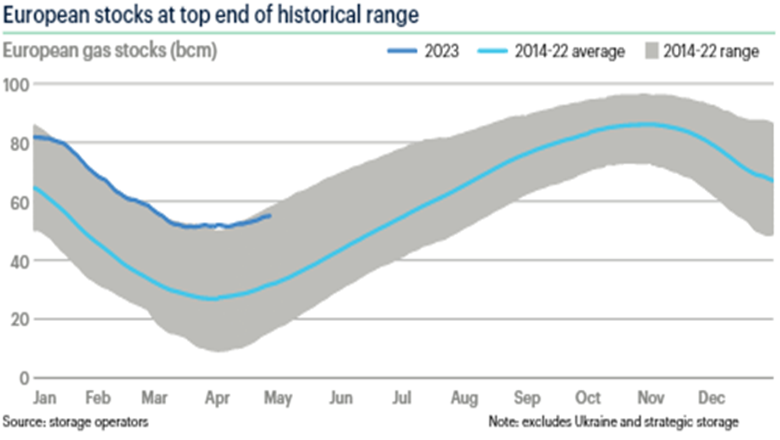

- EU aggregated storage levels were at an all time high in early April and they have remained at the higher end of historic averages throughout 2023 so far. See chart below, obtained from ICIS.

- However, gas injection rates have been reported to fall in recent weeks.

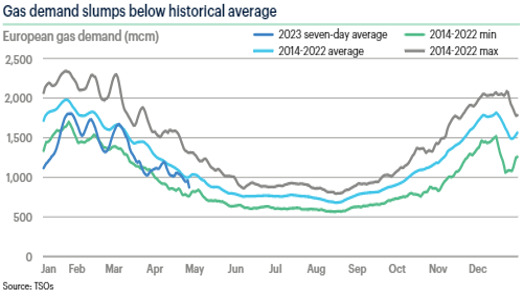

- Gas demand has been lower than average of late. See chart below, obtained from ICIS. This will help to get those storage sites filled up during refilling season.

- However, the question is now being asked; can gas injection rates of early 2023 be restored, in order to replenish stocks up to the required levels and see Europe safely through next winter?

Renewables

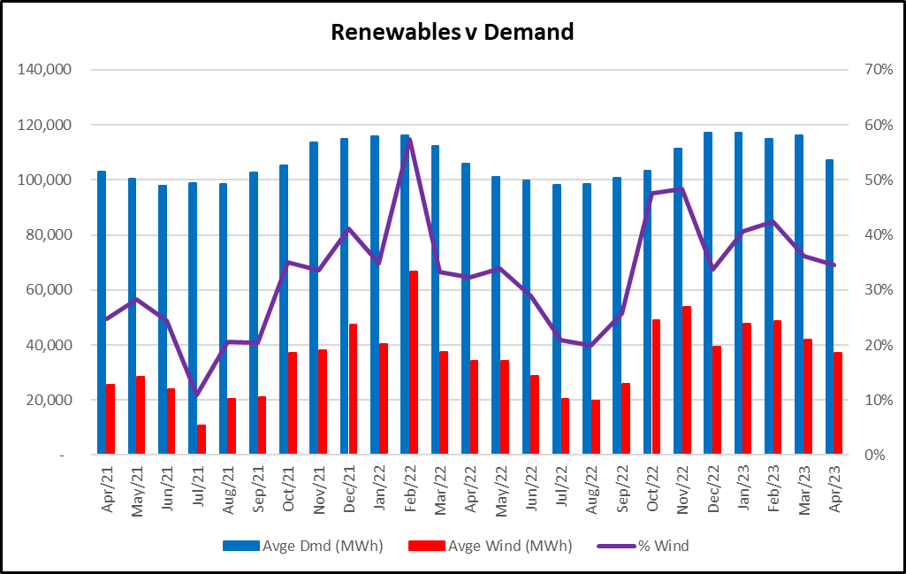

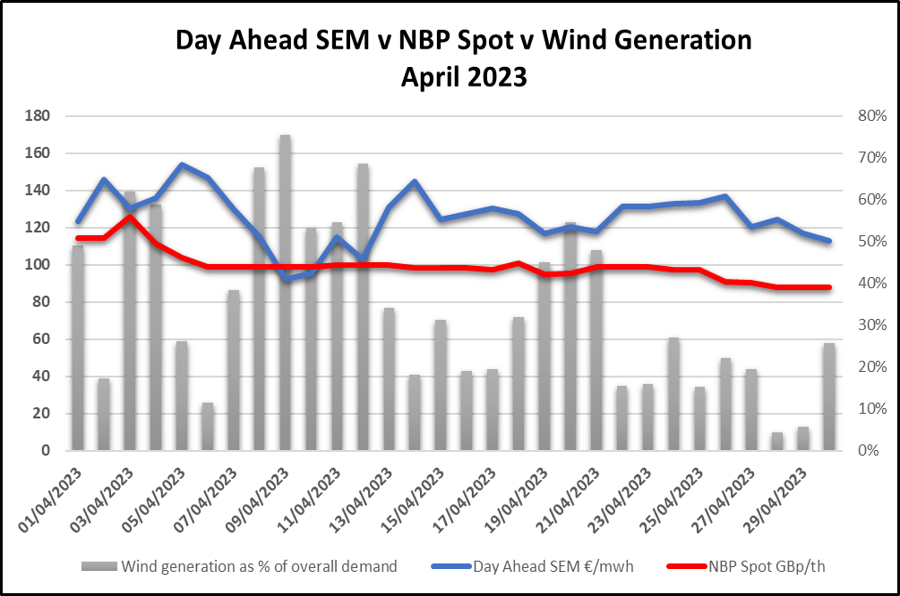

Renewables, in the form of wind, contributed an average of 35% of the Irish Generation Mix across April. See graph below.

As usual, when wind generation was up in April, the wholesale cost of power was generally lower. This common trend emphasises the importance of wind generation on the Irish power grid. See graph below.

Generation Capacity

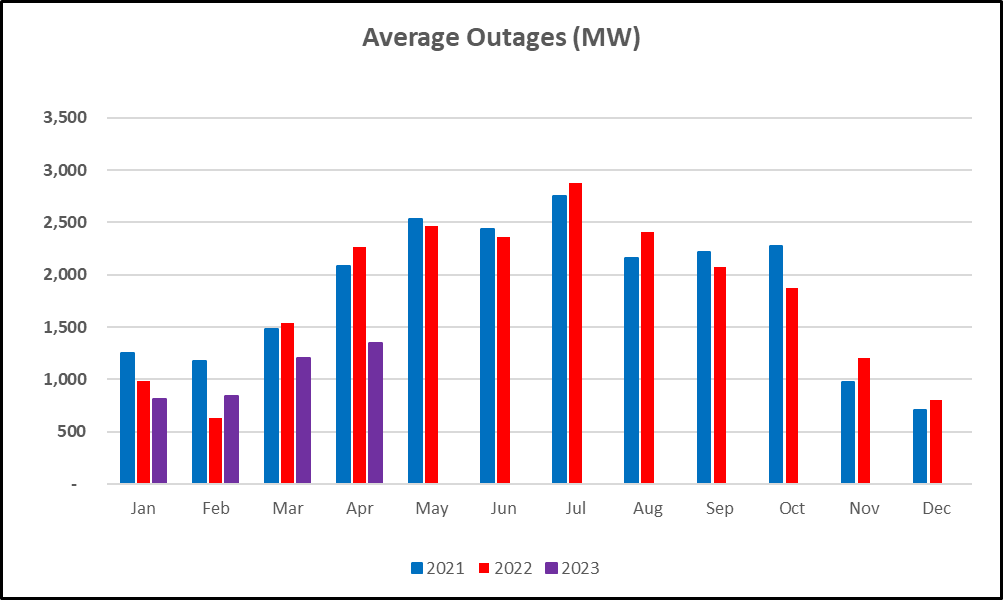

- Outages in April ‘23 were considerably lower than the previous two April periods.

Forecasts – Power Forward Prices

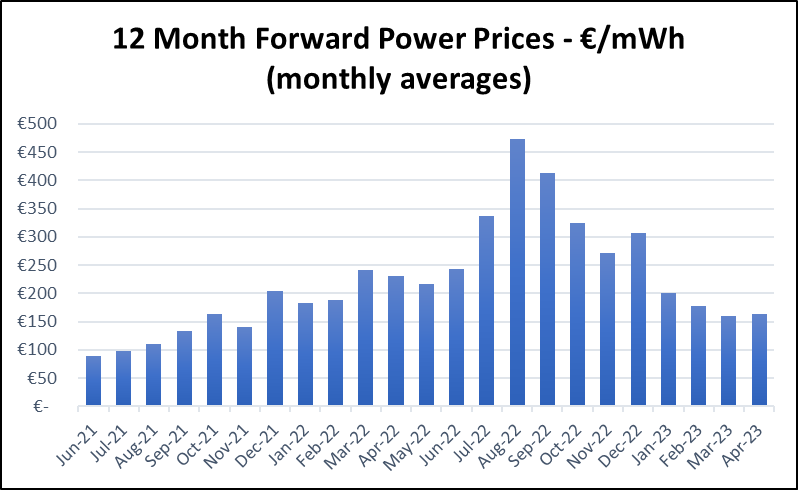

- Forward prices have fallen significantly since the turn of the year. They now seem to have levelled off somewhat, near the point they were at start of the energy crisis and before the invasion of Ukraine.

- As the dreadful war in Ukraine rumbles on, a high level of risk premium remains in energy markets. There are a number of factors at play, such as an uncertain international geopolitical situation and the newly evolving web of energy supply chains.

- Forward prices are now approximately 2.5x the previously accepted norms.

- It is key to understand that European buyers are now unwilling to sign the kind of long-term gas purchasing contracts that Asian countries are committing to. This is because current green energy targets suggest that overall gas requirement in Europe will fall significantly within this decade.

- This leaves European gas prices open to the risks of the international spot market for LNG. An elevated risk premium is sure to remain in forward power prices, such as those in Ireland, that are often determined by the price of gas generation.

- The heavier portion of that risk premium has now switched further out along the price curve, to 2024. However, some market participants have expressed caution on current 2023 price levels, noting a slow down of injection rates at gas storage sites recently.

- While EU gas storage levels are near all time highs, if injection rates are not restored to the required scale, this could cause another panic late in refilling season as sites push to reach 90% mandated gas storage levels.

- Global gas prices are expected to remain structurally high until at least 2026, after which there are a number of pending infrastructure projects due be completed, bringing more capacity online.

- These projects include Qatar’s North Field expansion and an assortment of new US LNG export projects, which have just recently entered construction.

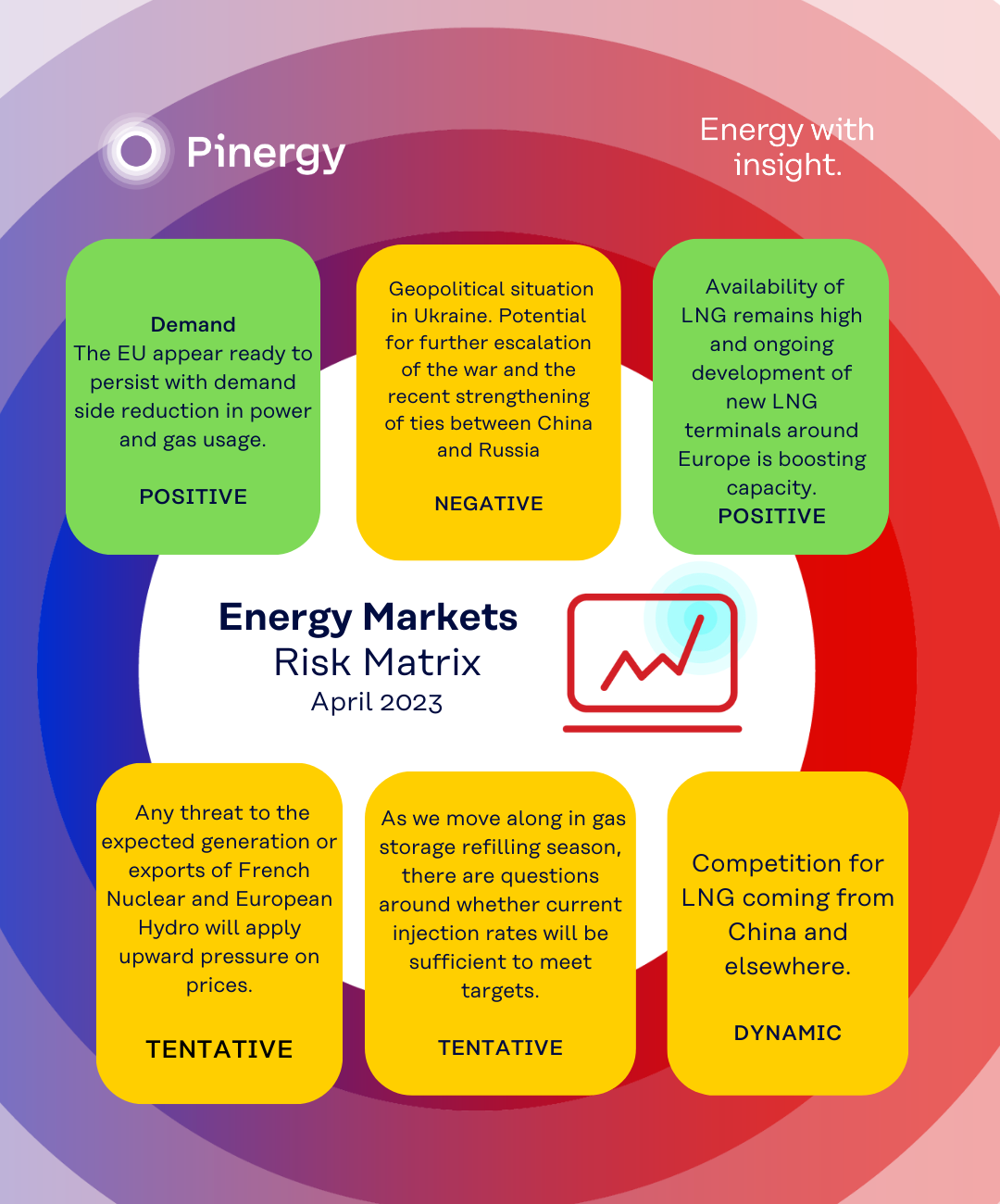

Pinergy Risk Matrix

We have compiled a list of the key factors we feel have the highest potential to influence power prices over the coming 12 months and rated as follows:

Green = Price reducing impact and highly probable.

Amber = Risk of increased power prices and of lower concern.

Red = Significant risk to 12 month forward price outlook, with medium to high probability.